|

服务热线:400-820-2536 |

|

服务热线:400-820-2536 |

2014年度企业所得税汇算清缴相应操作实务(苏州站)

2014年末,国家税务总局发布了“企业所得税年度纳税申报表”的公告,公布了修订后的《中华人民共和国企业所得税年度纳税申报表》于2015年1月1日开始施行,由于现行的“企业所得税年度纳税申报表”已经实施6年,在不少企业都已习惯的情况下,此次修订究竟改了哪些内容,企业应如何填写将是本次活动的重点关注。

本期价值要点:

l 2014年度汇算清缴新政变化解读

l 对企业所得税重要纳税事项进行全面梳理,避免漏掉重要调整项目

l 结合案例,讲解如何填制汇算清缴申报表

l 2014年企业所得税汇算清缴疑难问题解读

2014年度企业汇算清缴会员相关疑问(部分):

1.税局对于报表的修订究竟存在什么样的目的?为什么要这样修订?

2.表格之间的勾稽关系是怎样的? 可能企业填写时表面上看勾稽关系都是正确的, 但后台税局系统会提示预警, 将来引发税局对企业进行调查,如旧的申报表,企业对存货正常损失做了清单申报,但在附表三 资产类调整 项下 财产损失中未填列该 清单备案金额, 引发税局系统预警.

3.企业基础信息表 中 301企业主要股东(前5位)这里的股东是指 法人单位还是自然人?

4.期间费用明细表: 企业并没有对费用进行境内外的区分, 如何划分境内外费用?

5.职工薪酬纳税调整明细表 中的股权激励实际操作有何税务影响,能否帮助具体说明

6.2014年起,新增的研发设备100万以下的可以直接入费用, 该变更如何填写?

7.资产损失中,存货在生产过程中发生的正常损耗, 比如工单损耗,是否要做清单申报? 成品报废后当做废料出售了,是做清单申报还是专项申报?

8.境外代扣企业所得税的抵免如何计算与填列? 以前年度代扣且未在当年度抵扣的,是否可在以后年度计算抵免?

9.新申报表取消了关联交易表,为何取消?是否税局对关联交易有其他监控渠道 ? 取消该表,那么转移定价报告的关联交易数据如何勾稽?

本次活动关于相关汇算清缴报表填写

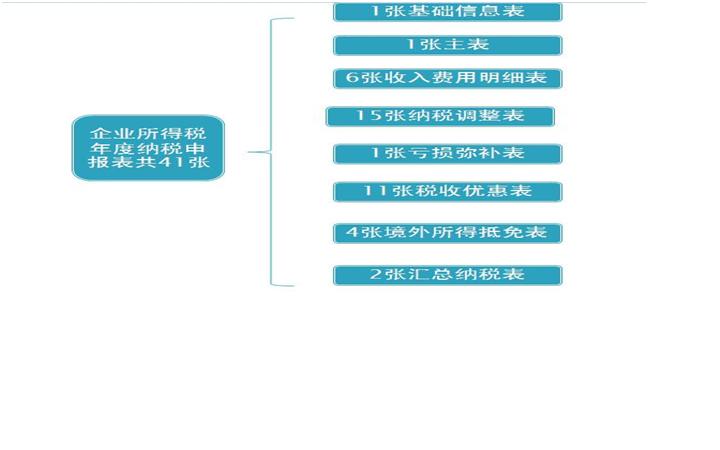

申请表的构成

现行是一张纳税调整表,修订后是15张纳税调整表,税局修订意义何在?

现行是1张税收优惠表,修订后是11张税收优惠表,税局修订意义何在?

活动特邀分享嘉宾

苏州所得税处官员

苏州德勤税务合伙人

流程安排

13:00-13:30签到

13:30-15:00 2014年汇算清缴新政解读,实操技巧及汇算清缴纳税筹划

l 解读2014年汇算清缴新政策

l 2014年优惠政策有哪些,如何申请应用

l 如何做好汇算清缴前的自查以及控制纳税风险

15:00-15:15 茶歇

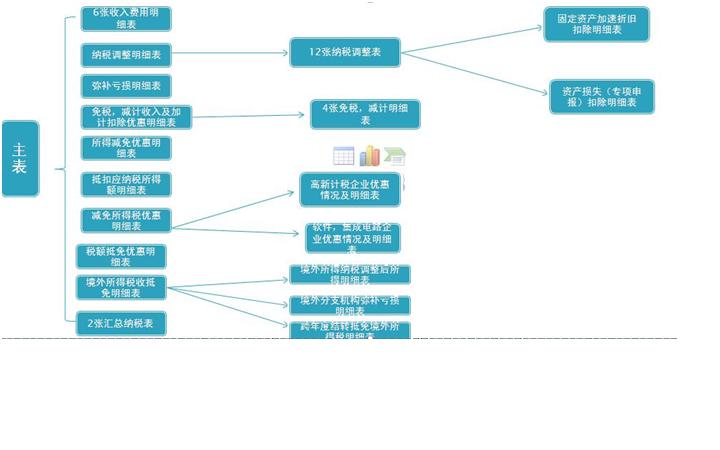

15:15-16:00企业所得税汇算清缴报表填写

l 封面

l 企业所得税年度纳税申报表填报表单的填写

l 企业基础信息表填写

l 中华人民共和国企业所得税年度纳税申报表(A类)填写

l 一般企业收入明细表填写

l 一般企业成本支出明细表填写

l 纳税调整项目明细科目讲解

l 专项用途财政性资金纳税调整表

l 职工薪酬纳税调整明细表

l 广告费和业务宣传费跨年度纳税调整明细表及案例解析

l 捐赠支出纳税调整明细表

l 资产折旧、摊销情况及纳税调整明细表

l 固定资产加速折旧、扣除明细表

l 企业所得税弥补亏损明细表

l 免税、减计收入及加计扣除优惠明细表

l 股息红利优惠明细表

l 抵扣应纳税所得额明细表

l 高新技术企业优惠情况及明细表

16:00-17:00企业所得税汇算清缴疑难问题解析

l 视同销售收入税收政策解析及纳税调整

——哪些业务被认为是视同销售

——视同销售金额如何确认

——视同销售业务税会差异及纳税调整分析

l 税法和会计容易产生争议的收入项目

——非货币性收入

——"买一赠一"

——一次性取得跨年租金收入

——政策性搬迁与处置收入

——股权转让所得

——不征税收入取得的利息

——财产转让

——处置资产

——不征税收入与免税收入

——几种特殊收入的确认时间

17:00-17:30 Q&A

17:30活动结束

2014企业所得税相关法规文件

1、国家税务总局关于企业所得税应纳税所得额若干问题的公告(国家税务总局公告【2014】年第29号)

2、【财政部】国家税务总局关于2014 2015年铁路建设债券利息收入企业所得税政策的通知(财税【2014年】2号)

3、国家税务总局关于商业零售企业存货损失税前扣除问题的公告---(财税【2014】年3号)

4、【财政部】国家税务总局关于小型微利企业所得税优惠政策有关问题的通知(财税【2014】年23号)

5、国家税务总局关于扩大小型微利企业减半征收企业所得税范围有关问题的公告(国家税务总局公告【2014】年第23号)

6、财政部 国家税务总局关于完善固定资产加速折旧企业所得税政策的通知(财税【2014】75号)

8、关于非营利组织免税资格认定管理有关问题的通知(财税【2014】13号)

9、关于小型微利企业所得税优惠政策有关问题的通知(财税【2014】34号)

10、关于继续实施支持和促进重点群体创业就业有关税收政策的通知(财税【2014】39号)

11、关于调整完善扶持自主就业退役士兵创业就业有关税收政策的通知(财税【2014】42号)

12、国家税务总局关于发布《电信企业增值税征收管理暂行办法》的公告(财税【2014】26号)

At the end of 2014, the state administration of taxation issued the "enterprise income tax return of the year", released the revised "law of the People's Republic of China on enterprise income tax the annual tax return" to start on January 1, 2015, as a result of the current "enterprise income tax return of the year" has been implemented six years, in the case of many enterprises have been used, the revision what exactly content changed, enterprises should focus on how to fill in will be the event.

Key Point

l 2014 annual liquidation new changes

l The comprehensive carding on the enterprise income tax important matters, to avoid missing important adjustment project

l Combined with the case, how to fill the income tax declaration form

l Enterprise income tax payable or refundable amount 2014 problems

2014 annual enterprise income tax members related question (part) :

l Did not set up trade union organization's enterprise according to the total wages 2% provision will prepare gold, 40% part to the local tax authorities to pay, by the taxation of the People's Republic of China general payment deducted before duty of enterprise income tax, and the remaining 60% for some businesses, no special union funds income receipt, 60% part can be deducted before duty of enterprise income tax?

l Enterprises have a decorate, modernize the amortization period since 5 years, amortization has two years, more than 3 years unamortized. Recently, the company decided to cancel the finished decorate unamortized modernize, can change the original amortization period, the remaining three years changed according to the remaining amortized over 1 year? After accelerated amortization, enterprise income tax can be deducted?

l Enterprises have a decorate, modernize the amortization period since 5 years, amortization has two years, more than 3 years unamortized. Recently, the company decided to cancel the finished decorate unamortized modernize, can change the original amortization period, the remaining three years changed according to the remaining amortized over 1 year? After accelerated amortization, enterprise income tax can be deducted?

l If the enterprise actual assets loss year for more than five years, but its accounting year took place in 2012, if the asset losses would declare and in the 2012 annual pre-tax deduction?

l Enterprise in the process of research and development for the collection, the developers also accrue to the r&d cost of travel range, at the same time, enterprises emphasize this is for research and development work in the field to verify the cost of exploration must occur, whether such travel can mutatis mutandis r&d cost in the range of the collection research and development, review and acceptance of argument, or should not accrue to the research and development within the scope of the account of the cost.

l Enterprise when carries on the recognition of hi-tech enterprises its total cost over the last three fiscal years of research and development accounts for the proportion of total sales revenue of not less than the corresponding standard is required over the last three fiscal years every year's research and development expenses are not less than the corresponding proportion of sales revenue or total expenses occurred nearly three year's research and development is no less than that of the corresponding percentage. For example, suppose a nearly three enterprise accounting annual sales income is 10 million yuan, for each year of research and development expenses amount to 450000 yuan, 600000 yuan and 800000 yuan, the company over the last three fiscal years research and development costs accounted for the proportion of total sales revenue of 6.33% of the total of no less than 6%. But this enterprise development costs for one of the annual sales revenue accounted for 4.5%, less than 6% of the proportion, the enterprise whether can meet the requirements of identified as high-tech enterprises.

Agenda

13:00-13:30 Sign

13:30-15:00 2014 settles the new interpretation, speaking skills and liquidation tax planning

l Reading settles the new policy in 2014

l What are the preferential policies, 2014 how to apply for application

l How to be refunded before the inspection and control of tax risk

15:00-15:15 Tea Break

15:15-16:00 The enterprise income tax payable or refundable amount filled in report

l Enterprise income tax the annual tax return completion of the form

l Enterprise basic information table to fill in

l Enterprise income tax of the People's Republic of China, the annual tax return (class A) to fill in

l General enterprise income sheet to fill in

l General enterprise cost sheet to fill in

l Pay taxes is adjusted project detail course

l Special purpose of fiscal fund tax adjustment

l Schedule of worker pay pay taxes is adjusted

l Advertising and business advertising purchase schedule of maximal tax adjustment and case analysis

l Donation schedule of spending tax adjustment

l Schedule of assets depreciation, amortization and tax adjustment

l Accelerated depreciation of fixed assets, the deduction list

l Schedule of enterprise income tax losses

l Tax exemption or reduction plan schedule of claim additional deduction income and preferential

l Schedule of preferential dividends

l Schedule of deduction of taxable income

l The favorable conditions and schedule of high-tech enterprises

16:00-17:00 Enterprise income tax income class project problems parsing

l As sales income tax policy and tax adjustment

- What kind of business is considered to be regarded as sales?

-How to identify - regarded as sales amount

- regarded as sales tax and tax adjustment analysis

l The tax law and accounting prone to dispute the income of the project

- Non-monetary income

-- "buy one send one"

- a one-time get across to rent income

- Policy move and disposal income

- Equity transfer income

-- No tax income of interest

- Property transfer

- The disposal of the asset

-- No tax income and tax revenue

- Some special income confirmation time

17:00-17:30 Q&A

17:30End

| 客服专线:400 820 2536 | 咨询专线:400 820 2536 |

| 咨询邮箱: | 解答邮箱:cs@fcouncil.com |

银行名称:招商银行股份有限公司

开户行:招商银行股份有限公司上海虹桥支行

帐户:121908638710202

|

Copyright © 2008-2026 协同共享企业服务(上海)股份有限公司版权所有 China Finance Executive Council (F-Council)为协同共享企业服务(上海)股份有限公司旗下服务品牌 网站备案/许可证号:沪ICP备15031503号-1 |

FCouncil |

御财府 |

||||